Massachusetts Health Insurance - Metal Tiers, Minimum Essential Coverage, and Out-Of-Pocket Maximums

If you are looking for Massachusetts health insurance, you have several options. Read this article to learn about Massachusetts health insurance metal tiers, minimum essential coverage, and out-of-pocket maximums. In addition, find out how to access physicians and hospitals. Then, choose the best plan for you.

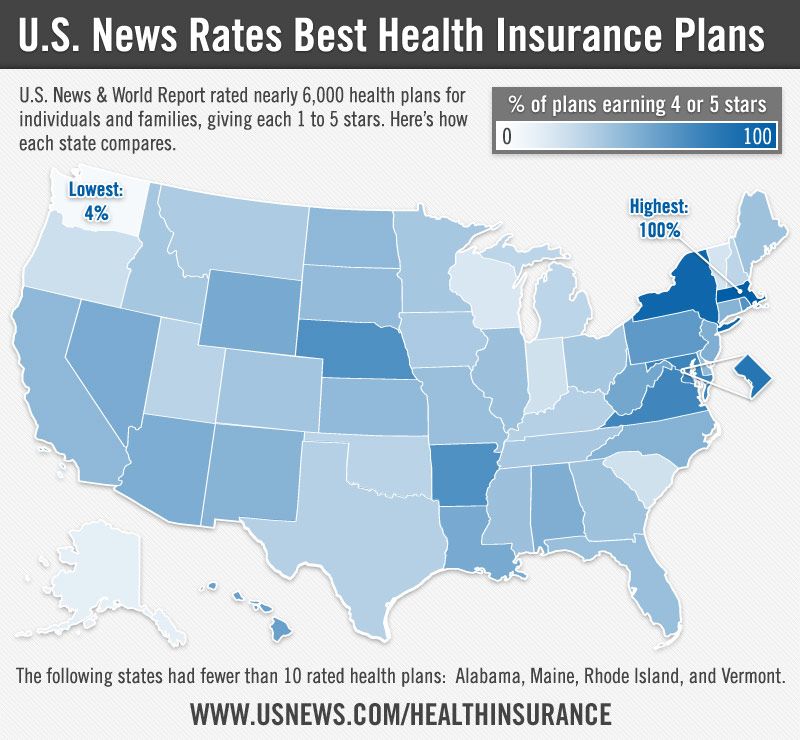

Metal tiers of Massachusetts health insurance

Massachusetts health insurance plans are divided into four metal tiers based on their cost and level of coverage. Each tier has different benefits, and you can decide which is best for your situation. The right tier depends on your age, your health, and your family situation. A younger individual will not need a higher tier, while a family with children will probably want a lower one. A higher tier will cover more expenses but cost more in monthly premiums.

The first step to choosing a health plan is to assess how much you can afford to pay. A higher tier will be the best option if you need comprehensive medical care and can afford a higher premium. You can select a lower tier to save money if you don't need as much medical care.

Minimum essential coverage requirements

Minimum essential coverage requirements for Massachusetts health insurance are key to the state's health care reform. In 2008, 2.6 percent of the state's population was uninsured. Massachusetts health reform was implemented to reduce this rate and improve access to health insurance. Its success depends on the willingness of stakeholders to accept the new coverage requirements and the affordability of premiums. Massachusetts' reform model also requires insurance regulators and policymakers to ensure that insurers comply with these new requirements.

Unlike minimum essential coverage in other states, Massachusetts requires health insurance plans to meet certain standards. To qualify for the health insurance exchange, an insurer must provide 10 essential health benefits and follow federal cost limits. Qualifying health plans can be employer-sponsored, individual major medical plans, Medicaid, CHIP, or Medicare. They must also cover preventive care, prescription drugs, and pregnancy.

Out-of-pocket maximums

In 2006, the state of Massachusetts enacted a comprehensive health reform initiative that was based on the shared responsibility principle. This plan expanded the Medicaid program and created a new subsidized program through a health insurance exchange. It also reformed the health insurance market, establishing a minimum requirement for individuals to have insurance. Massachusetts also imposed a mandate on employers that did not offer insurance. This reform program was the first in the country to require individuals to have health insurance coverage.

The Affordable Care Act allows Massachusetts residents to enroll in health insurance plans for a reduced premium. Many people with a high-cost health insurance policy can take advantage of tax credits and special enrollment periods. Many of these plans are also available to people with low incomes. Some Massachusetts health insurance plans are subsidized with federal and state funds. The premium tax credits and cost-sharing subsidies will help you lower your out-of-pocket maximums if you qualify for MassHealth.

Access to doctors and hospitals

The Massachusetts health insurance reform program has reduced the number of uninsured residents, but its effect on access to physicians and hospitals may not be universal. In addition, some studies have found that cost-related barriers may limit access. Furthermore, the types of insurance available to newly insured residents may not facilitate access as much as employer-sponsored insurance.

One of the key differences between health insurance policies in Massachusetts is how much coverage is provided. A Massachusetts health insurance plan will provide coverage for hospital stays, prescription drugs, and doctor visits. While many plans require a copay, Massachusetts plans will cover most of the costs.